See you in 2012!

We’re coming to the end of another wonderful year. It has been such an extraordinary pleasure to work with each of you in 2011, and I am looking forward to what next year will bring for us. I have never been more sure that this company is built on quality, not quantity, than when I […]

Source: http://www.hassonblog.com/2011/12/see-you-in-2012/

credit history escrow lien condominium government loan (mortgage) judgment maturity

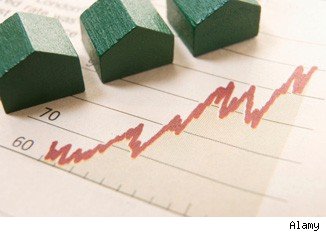

Locking In Peace of Mind

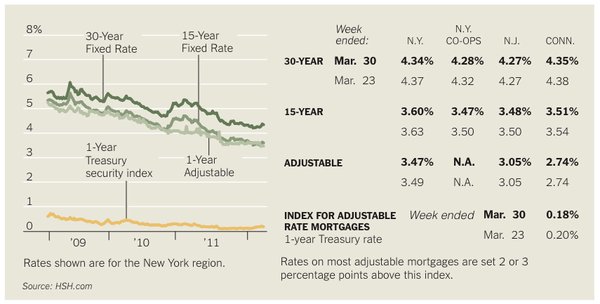

WITH mortgage rates inching higher, some borrowers might want to consider a lock-in agreement, which freezes the terms of a loan while it is being processed, potentially saving borrowers thousands of dollars over the life of the mortgage.

This guarantee may be especially important for those who are refinancing, where even a quarter of a percentage point could skew a borrower’s calculations and make a refinancing less financially desirable, said Keith T. Gumbinger, a vice president of HSH.com a financial publisher in Pompton Plains, N.J.

Rates for the 30-year fixed-rate mortgage averaged 3.95 percent nationwide in March, up from 3.89 percent in February, according to Freddie Mac, though that is still significantly lower than the 4.84 average rate in March 2011. The average rate was 3.98 percent on Thursday, versus 3.99 percent the week before.

“We expect fixed-rate mortgages to gradually move higher over the next six months to about 4.25 to 4.5 percent as the country’s economic condition improves,” said Frank Nothaft, Freddie Mac’s vice president and chief economist. “This would be a move from the all-time record low rates we’ve experienced over the last few months but still at historically low levels.”

Rate lock-ins can provide buyers with some peace of mind, not to mention one less thing to think about in an otherwise onerous application process.

Lenders typically will give loan rate guarantee agreements when a borrower has a purchase agreement, but a few will provide them to those who are preapproved for a mortgage, said Rick Allen, the chief operating officer of Mortgage Marvel, an online site.

While shopping for a mortgage lender, Mr. Allen suggests inquiring about loan locks, too. “Get a copy of the rate lock agreement,” he said, noting that this would help borrowers better understand how the process works.

The cost of reserving an interest rate depends both on the duration of the lock and the amount of the loan. “The longer the lock, the more costly it is,” said Mark Lazar, an owner of Allied Financial Mortgage in River Edge, N.J. Most locks are for 30, 45 or 60 days, but some lenders will go as long as six months.

Most lenders offer some version of a free lock, Mr. Gumbinger said, though it may be only for 30 days. Others charge points — or fractions thereof — based on the loan size, which could amount to several hundred dollars. (A point is equal to 1 percent of the loan amount.) Sometimes these charges are refundable at closing, Mr. Gumbinger said.

promissory note purchase agreement no cash-out refinance seller carry-back planned unit development (PUD) down payment subdivision

Joe Paterno’s Real Estate Transfer: Suspicious or Not?

Filed under: News, Advice, Celebrity Homes, Other

Why would former Penn State football coach Joe Paterno transfer ownership of his house, worth $594,484, to his wife for $1 in July, unless he knew that he was about to be drawn into the college’s sex-abuse scandal, with potential civil lawsuits and damages heading upfield toward him?

While his lawyer told The New York Times that the ownership transfer was nothing more than a step in a long-term financial estate plan, the move raised some eyebrows. Was the sale an attempt by Paterno to shield assets, fearing that some jury down the road might take him to the cleaners? And by transferring his home to his wife, Sue Paterno, did the coach who once walked on water just sink deeper into the dark hole of public scorn?

AOL Real Estate spoke to several estate lawyers and heard pretty much the same thing: Joe Pa probably didn’t do anything fishy, at least when it came to giving his wife the house for $1 plus “love and affection.” The couple (pictured at left) had previously held joint ownership of the property, for which they paid $58,000 in 1969.

AOL Real Estate spoke to several estate lawyers and heard pretty much the same thing: Joe Pa probably didn’t do anything fishy, at least when it came to giving his wife the house for $1 plus “love and affection.” The couple (pictured at left) had previously held joint ownership of the property, for which they paid $58,000 in 1969.

David Shulman, an attorney in Fort Lauderdale, Fla., whose practice focuses on trusts and estates, says there’s no obvious reason to link the home transfer with an attempt to protect assets or do an end-run around prospective creditors. In Pennsylvania, Shulman noted, as long as the property is held jointly — as Paterno’s was — it can’t be subject to the creditors of just one of the spouses. And since Sue Paterno hasn’t been linked at all to the sex-abuse scandal, she has no liability or exposure.

“I haven’t seen the documents,” Shulman said, “but from what’s been made public, it just doesn’t make any sense that this was an attempt to protect assets.”

Then what was Paterno up to? Shulman said the 84-year-old Paterno’s decision to transfer the house more likely had something to do with age-related issues, such as Medicaid and tax planning. To qualify for Medicaid-covered nursing home care, for example, a recipient must “spend down” to a certain level. And people are constantly looking to protect their assets from taxes to ensure that their heirs inherit as much as possible.

Since Paterno has good insurance and a degree of wealth, he probably didn’t do it for Medicaid purposes. Far more likely it was done as an estate planning move to avoid probate, said Shulman. “It is a fairly typical thing for people of means to want to protect their assets for their children or whoever will inherit them,” he said.

Paterno, who was fired as the football coach at Penn State, has been harshly criticized by many for not taking more aggressive steps after a suspected sexual assault of a child by one of his former top assistants was reported to him. And if the reaction to the house transfer is any indication, it’s a safe bet that the burgeoning scandal will cast suspicion on everything else the coach does.

[Correction: An earlier version of this post incorrectly referred to Paterno as Joe Pop; his nickname is Joe Pa.]

Also see:

Taking a Tax Loss When Property Value Declines

Happy End of the Road for RVers: Assisted Living on Wheels

%Gallery-138464%

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find rentals in your area.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2011/11/16/joe-paternos-real-estate-transfer-suspicious-or-not/

lease purchase money transaction closing costs public auction servicing FHA mortgage Equal Credit Opportunity Act (ECOA)

30-Year Mortgage Rate Falls to Another Record Low: 3.66%

Filed under: News, Refinancing

By Marcy Gordon

By Marcy Gordon

WASHINGTON — The average U.S. rate on a 30-year fixed mortgage fell this week to a record low for the seventh time in eight weeks. Cheap mortgages have helped drive a modest recovery in the weak housing market this year.

Mortgage buyer Freddie Mac said Thursday that the average on the 30-year loan dropped to 3.66 percent. That’s down from 3.71 percent last week and the lowest since long-term mortgages began in the 1950s.

The average rate on the 15-year mortgage, a popular refinancing option, declined to 2.95 percent. That’s down from 2.98 percent last week and just above the record 2.94 percent reached two weeks ago.

The rate on the 30-year loan has been below 4 percent since December.

Low rates could provide some help to the economy if more people refinance. When people refinance at lower rates, they pay less interest on their loans and have more money to spend.

Still, the pace of home sales remains well below healthy levels. Sales of previously occupied homes dipped in May to a seasonally adjusted annual rate of 4.55 million, although they are up from the same month last year.

Many people are still having difficulty qualifying for home loans or can’t afford larger down payments required by banks. Some would-be home buyers are holding off because they fear that home prices could keep falling.

The U.S. economy is growing only modestly and job creation slowed sharply in April and May. U.S. employers created only 69,000 jobs in May, the fewest in a year.

Mortgage rates have been dropping because they tend to track the yield on the 10-year Treasury note. Uncertainty about how Europe will resolve its debt crisis has led investors to buy more Treasury securities, which are considered safe investments. As demand for Treasurys increase, the yield falls.

And the yield will likely fall even lower now that the Federal Reserve has said it will continue selling short-term Treasurys and using the proceeds to buy longer-term Treasurys. That goal of the program is to drive long-term interest rates lower to encourage more borrowing and spending.

To calculate average rates, Freddie Mac surveys lenders across the country on Monday through Wednesday of each week.

The average does not include extra fees, known as points, which most borrowers must pay to get the lowest rates. One point equals 1 percent of the loan amount.

The average fee for 30-year loans was 0.7 point, unchanged from last week. The fee for 15-year loans was 0.6 point, down from 0.7.

The average rate on one-year adjustable rate mortgages fell to 2.74 percent from 2.78 percent last week. The fee for one-year adjustable rate loans was unchanged at 0.5 point.

Copyright 2012 The Associated Press. The information contained in the AP news report may not be published, broadcast, rewritten or otherwise distributed without the prior written authority of The Associated Press. Active hyperlinks have been inserted by AOL.

See also:

5 Things That Can Derail Your Home Sale

Home Affordability: How Much House (or Apartment) Can I Handle?

Home Costs: 4 Crucial Questions Reveal Hidden Expenses

%Gallery-158199%

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/06/21/30-year-mortgage-rate-falls-to-record-low/

rate lock fair market value common law cap right of first refusal loan-to-value (LTV) appraised value

When It Comes to Mortgages, Women Don’t Shop Enough

Filed under: News, Advice, Financing, Refinancing

There’s a surprising new finding that says women get lousier mortgage rates than men, but not because of gender discrimination. It’s because instead of shopping around for cheaper loans, they rely on the recommendations of friends.

To recap: When it comes to mortgages, women don’t shop enough.

The report published in the Journal of Real Estate Finance and Economics set out to explain why women were 32 percent more likely to get a subprime mortgage than men in a 2006 study. According to a team of researchers led by Florida Atlantic University’s Ping Cheng, the answer wasn’t discrimination because of gender or even income disparities.

Women pay higher rates because they are more likely to listen to friends’ recommendations, whereas men are more likely to shop around for the best deal.

“Our empirical test confirms that search effort is rewarded in marketplace, and suggests that gender disparity in mortgage rates may be addressed by policies aimed at improving women’s financial literacy and search skills,” the report summarizes.

It makes sense to Daily Finance columnist Laura Rowley. “It’s not surprising, because mortgage shopping can be incredibly complex, so we look to people we can trust to help make the decision,” says Rowley. “But this is one area where you don’t want to get by with a little help from your friends.”

Instead, she advises, call two mortgage brokers and a direct lender, preferably a local small or mid-size bank, and try the following script: “Hi, my name is ____ and I’m in the market to buy a $____ house, and I’m going to put down ____ percent. I’m getting three written estimates, and then I’m going to choose. Can you email me a cost-estimate worksheet stating all the fees and the interest rate?”

Be sure to get the estimates on the same day, as rates can change quickly. Also, don’t ask for rates and fees by phone; unscrupulous brokers will simply low-ball their estimate to get you in the door, says Rowley.

For more tips on shopping for a mortgage, see these AOL Real Estate guides:

How Much Can You Afford [Video]

How to Get a Low Mortgage Rate

Mortgage Jargon in Simple Terms

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

See celebrity real estate.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2011/11/18/when-it-comes-to-mortgages-women-dont-shop-enough/

right of first refusal loan-to-value (LTV) appraised value escrow account grantee Government National Mortgage Association (Ginnie Mae) closing

1 in 4 Spend More Than Half of Income on Housing, Study Says

In the wake of the housing bust, almost 1 in 4 working families spend more than half their income on housing costs, according to a new study.

In the wake of the housing bust, almost 1 in 4 working families spend more than half their income on housing costs, according to a new study.

The study by the Center for Housing Policy found that both homeowners and renters continue to struggle with housing costs since the market tanked in 2008. Between 2008 and 2010, renters saw their median income decline even as housing costs rose, while homeowners’ loss of income outpaced a modest drop in housing costs. Experts typically warn against using more than 30 percent of pretax income toward housing costs. (Read more about debt-to-income ratio here.)

In 2010, the latest year in which data was available, there were 10.6 million households with more than half their income going toward housing, including utilities. A total of 23.6 percent of working households fell into that precarious category — up 1.8 percentage points from 2008. (The study defines working households as those that make less than 120 percent of an area’s median income and work at least 20 hours a week.)

With prospective buyers finding it harder to qualify for a mortgage and job security remaining a top concern for many families, rental demand has surged in past years, driving up costs. For homebuyers who purchased risky loans with little equity at stake during the boom years, high interest and sliding home values have pushed thousands underwater, with insufficient savings to escape the cycle.

%Gallery-139166%

“The data show that homeowners have been hit hard by the housing crisis in more ways than just lost equity,” said Jeffrey Lubell, executive director at the Center for Housing Policy, in a statement. “Many working homeowners have been laid off or had their hours cut.”

Homeowners felt the pinch of diminishing salaries more acutely than renters, dropping to a median of $41,413 in 2010, down from $43,570 in 2008. Working renters, on the other hand, typically make less, with a median income of $30,229 in 2010.

Unsurprisingly, the groups that were most at risk of having a severe housing cost burden made less than 80 percent of their area’s median income, whereas wealthier households held steady over the 2-year period.

Where Housing Hurts Most

Between 2008 and 2010, affordability has significantly declined in 24 states. The five states with the highest share of households spending more than half their incomes on housing were California (34 percent), Florida (33 percent), New Jersey (32 percent), Hawaii (30 percent) and Nevada (29 percent).

With several experts predicting that the $25 billion mortgage settlement with the nation’s largest banks will lead to more foreclosures at the start of 2012, both renters and owners should brace for more price fluctuation in their local markets, at least in the short term.

That said, the group most affected by the price confusion are those who bought during the height of the housing bubble, prior to 2008. For those entering the market today, however, sinking prices and near-record low mortgage rates places home affordability at a 20-year high.

Also see:

Black Borrowers Face Higher Hurdles in Lending, Study Shows

How the Foreclosure Settlement Could Affect You

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find rentals in your area.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/02/27/1-in-4-spend-more-than-half-their-income-on-housing-study/

mortgage broker recorder subordinate financing fee simple payment change date title insurance mortgagor

Viewpoint: Where’s Housing in the ‘Occupy’ Protests?

Filed under: News, Economy, Foreclosures, Credit

Did the voices of the housing crisis just get swallowed up by the anti-Wall Street protests? Marches, sit-ins and confrontations with police — all part of the Occupy Wall St. movement that organizers say was birthed organically and fed through social media outlets — are happening in major cities across the country. Without question, windows across America have opened and, just like in the movie “Network,” people are shouting “I’m mad as hell and I’m not going to take it anymore!”

The only problem is that homeowners caught in the foreclosure crisis also stuck their heads out those windows and save for a fleeting few seconds, the take-to-the-streets protests have ignored them in favor of taking corporate greed to task. Nowhere on the main Occupy Wall St. website is housing even mentioned. (Pictured above are protesters in Los Angeles.)

Before you accuse us of wearing blinders, it’s worth noting that just a few weeks ago, a coalition of community groups called The New Bottom Line organized a nationwide 10-city protest aimed at stopping foreclosures, demanding that banks reduce principal loan amounts of all underwater mortgages and that Wall Street stop hoarding the trillions of dollars it got in stimulus money and start funding small business’ efforts to create jobs. Hallelujah to that, we say.

Seeing commonality with the Occupy Wall St. troops, The New Bottom Line demonstrators have joined forces with the faster-spreading Occupiers. The New Bottom Line co-director Tracy Van Slyke says that the excitement generated by the larger protests taking place will transfer energy — over time — to relief for housing. Let’s hope so. The millions of displaced families who lost their homes to foreclosures deserve a voice shouting on their behalf.

Where The New Bottom Line had been focused on the housing struggles facing the lower and middle class, Occupy appeals to a younger demographic — those hard hit by rising unemployment and emotionally about as far away from losing a family home to foreclosure as you can likely be.

About all they have in common is anger, which ultimately may be enough.

Also see:

Foreclosed Homeowner ‘Booby-Traps’ Home

Realtors’ Latest Challenge: A Surge of Squatters

Foreclosure Rescue Scammers Busier — and Trickier — Than Ever

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

See celebrity real estate.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2011/10/05/viewpoint-wheres-housing-in-the-occupy-protests/

cash-out refinance depreciation merged credit report second mortgage qualifying ratios easement PITI

Loan Thaw? Average Mortgage Up by $20,000, Study Says

The average loan size that lenders issued to borrowers in the past three months grew by $20,000, suggesting a thawing in mortgage lending, Capital Economics said Wednesday.

While the report, which was released by Capital Economics analysts Paul Dales, Paul Diggle and Amna Asaf, stopped short of calling the good news a full lending recovery, Dales said, “it may be an early sign that buyer confidence is improving.”

In 2012, the average amount of a mortgage went from around $215,000 to $235,000. The higher loan amounts are not the only positive economic indicator highlighted by the research firm.

Capital Economics reported a 20 percent drop in visible home inventory over the past 18 months, resulting in a situation where a months’ supply of unsold homes is now at a level where existing home sales can support current prices. At the same time, Capital Economics believes there are currently 3.9 million homes in the nation’s shadow inventory.

%Gallery-146461%

Even though employment numbers fell below the average analyst’s expectation of 200,000 new jobs in March, Capital Economics is more optimistic with the current three-month new jobs average sitting at 212,000 positions.

“We are not too alarmed by the 120,000 rise in payroll employment in March, which was exactly half the 240,000 gain in February,” Dales wrote. “Just as the unusually mild weather meant that employment grew at a faster rate than the underlying trend in the previous few months, it may now be growing at a slower rate than the underlying trend.”

Even though mortgage rates grew slightly in March, Capital Economics said the uptick will have little effect on housing activity since prices still remain affordable and undervalued.

The researchers believes there are signs in the market of a price bottom, but said significant home price gains are not expected in the near term since tighter lending restrictions are prohibiting a boom in real estate activity.

Read more on HousingWire:

Fannie, Freddie and the FHA Lead Surge in Multifamily Lending

Mortgage Applications Fall 2.4% as Purchases, Refinances Decline

RealtyTrac: Foreclosure Filings Fall to 4Q 2007 Level

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

See celebrity real estate.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/04/12/home-loan-thaw-average-mortgage-up-by-20-000-study-says/

encumbrance vested call option acceleration clause cash-out refinance depreciation merged credit report

Where Are the Real Home Bargains? Not Where You Think!

Filed under: News, Advice, Buying, Financing, Foreclosures, How To, Investing, Renting, Selling

What if you could buy a house for $25,000 in a neighborhood that wasn’t a battle-scarred slum and rent it out for $750 a month as soon as the ink was dry on the deal? Where are these deals that let you recapture your investment in just three years and from then on enjoy a steady monthly income from the property?

If you said Phoenix, Las Vegas or south Florida, you’d be wrong says Paul Habibi, a principal of Habibi Properties and real estate professor at UCLA Anderson School of Management.

Here’s a hint to the place Habibi thinks is the hottest investment around.

Yep, Habibi is humming “Kansas City” right along with Wilbert Harrison, Fats Domino and the 50 or so other recording artists who covered that tune. As for a real estate investment, Habibi says Kansas City, Mo., is ripe for the picking.

Habibi’s approach to real estate deals is not for novice investors, but it is for those who can tolerate some risk and buy into a statistician’s mind. He’s developed a matrix that filters the top 30 MSAs (metropolitan statistical areas) through their projected growth rates (increasing population is good), unemployment (the lower, the better), and whether the city has a diversified job platform (Silicon Valley won’t get his money).

He also rejects places where other investors have already scooped up the bargains (forget Florida and Las Vegas). Phoenix, popular with many investors, also fails his litmus test. It was built as a retirement community and lacks a job infrastructure for future growth, he says. And those Texas cities that everyone bandies about — Dallas, Austin, San Antonio — while their prices have remained flat and they seem to have escaped relatively unscathed from the recession, there are so many investors already there that they’re tripping over one another.

Kansas City is just about perfect, said Habibi, whose company recently concluded its first phase of buying 32 single-family homes there in “C-level” neighborhoods for a price point of $25,000 each, spent $5,000 to $10,000 on repairs and now rents them out for about $750 each. He expects to double or triple his holdings in Kansas City with his second investment fund, for which there is a minimum buy-in of $100,000 for accredited investors to participate.

Kansas City’s population grew at a faster-than-national average pace from 2000 to 2010. With an unemployment rate of 8.7 percent, it falls below the national level of unemployment of 9.1 percent. The city has a diversified industry base that includes Sprint Nextel Corporation, Hallmark Cards, the Fort Leavenworth military base, UPS and a Ford assembly plant. Google has selected the city for its ultra high-speed broadband network project. Plus Kansas City has a business-friendly reputation for encouraging retention of companies.

Habibi discourages individual investors without much experience or tolerance for risk to try to fly solo. He credits much of his success from having an infrastructure in place — people to scout and inspect the homes, screen for tenants, manage the properties on-site and swiftly deal with eviction issues.

For those who don’t want to listen to the expert, click on the images below of some homes for sale in the Kansas City area that are worth checking out:

See other homes for sale in the Kansas City area at AOL Real Estate.

Also see:

College Town Real Estate Investments Score High Marks

Upside Down on Your First House? Just Buy a Second One!

Viewpoint: Why No New Houses May Be a Good Thing

%Gallery-137999%

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find rentals in your area.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2011/11/02/where-are-the-real-home-bargains-not-where-you-think/

private mortgage insurance (MI) leasehold estate no-cost loan mortgage banker bond market servicer appraisal

BarterQuest How-to: Trade Smart at the Best Bartering Site

If you’re into bartering, chances are you’ve discovered BarterQuest a relatively new site that helps folks trade one product or service for another — like eBay but without cash. BarterQuest also makes multi-party trades easy, so you don’t have to find that one person looking for the exact thing you have, you can do three way (or more) swaps.

The post BarterQuest How-to: Trade Smart at the Best Bartering Site appeared first on DailyPerk.

Source: http://dailyperk.perkstreet.com/barterquest/

home inspection lock-in period trustee effective age credit repository loan servicing legal description

Paul Ryan Favors Dissolving Fannie Mae, Freddie Mac

Filed under: News, Financing, Election 2012

A Mitt Romney administration plan for a future housing finance system likely shuns any form of a government guarantee, based on the Republican presidential candidate’s choice of Rep. Paul Ryan as a running mate.

The Republican congressman from Wisconsin, who heads the House Budget Committee, released a plan that was passed by the House last year to slash spending across nearly every sector of the government, excluding the military. Ryan’s plan has received renewed attention after Romney, the Republicans’ presumptive presidential nominee, announced Saturday that Ryan was his pick for vice president. Democrats are looking to target specifics from the Romney campaign while Republicans are hoping to recharge their base.

Romney’s selection of Ryan also gives markets much needed insight into how the former governor of Massachusetts would proceed with a long-anticipated reform of the government-sponsored enterprises. The long-term outlook of the Ryan plan involves a complete wind-down of Fannie Mae and Freddie Mac and an end to their bailouts — which have cost $188 billion so far.

The Ryan budget would “privatize the business of government-owned housing giants, Fannie Mae and Freddie Mac, so they no longer expose taxpayers to trillions of dollars’ worth of risk.”

Read the rest of this story at HousingWire.

See also:

Freddie Mac Posts $1.2 Billion Net Income in 2nd Quarter

High-End Homeowners Racing to Sell Before Tax Cuts End

Michigan Man Buys County’s Entire Foreclosure Stock

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/08/14/paul-ryan-favors-dissolving-fannie-mae-freddie-mac/

lien condominium government loan (mortgage) judgment maturity margin tenancy in common

Mortgage Principal Reduction on Freddie Mac Loans?

By Jon Prior

By Jon Prior

Freddie Mac CEO Charles “Ed” Haldeman gave a strong signal Friday that new incentives from the Treasury Department may be enough to start principal reduction on mortgages backed by the government-sponsored enterprises.

In January, the Treasury said it would triple incentive payments to mortgage investors who allow principal reduction in Home Affordable Modification Program workouts. The payouts ranged between six and 21 cents to the investors for each dollar forgiven under HAMP, but that will grow to between 18 and 63 cents.

“I have to say recently the Treasury sweetened the program and tremendously increased the incentive payments in their offer to us,” Haldeman said at HousingWire’s REThink Symposium. “We will reevaluate that to see what may be in our economic best interest. If there are very large incentive payments — which could be 50 percent of what you could write down — it may be in our economic self-interest to participate in that.”

There are currently 11.1 million borrowers who owe more on their mortgage than the house is worth, according to CoreLogic. Of that, estimates show roughly 3.3 million of those mortgages belong to Fannie and Freddie.

The GSEs and their regulator, the Federal Housing Finance Agency, long shunned principal reduction. Their biggest fear is moral hazard — that borrowers who are still current on their underwater loan would strategically default in order to get principal written down.

“We thought principal reduction could have unintended, secondary consequences on other borrowers seeking the same kind of reduction,” Haldeman said.

One previous analysis showed the GSEs would take significant credit losses if a wide-scale program was put in place. A new analysis from the FHFA, which would cover the new HAMP incentives, is expected to be released in the coming weeks.

NPR and ProPublica reported Friday that the analysis will show a reversal, that principal reduction will work for the GSEs under the new version of HAMP.

“As we complete the review, the public should understand that Fannie Mae and Freddie Mac continue to offer a broad array of assistance to troubled borrowers and have continued to implement HARP 2.0 to enhance refinancing opportunities for underwater borrowers,” FHFA said in a statement.

Treasury Secretary Timothy Geithner told a House panel this week he and FHFA Acting Director Edward DeMarco were working out their differences.

Haldeman, who announced in October that he would leave his post at Freddie, said the principal reduction verdict will ultimately reside with DeMarco, but he isn’t operating on his own.

“At the end of the day, we are in conservatorship, and he is the conservator. But the way it works on a day-to-day basis is that it’s a very close collaboration. It is extremely rare that I had a different point of view than Ed DeMarco,” Haldeman said.

Read more on HousingWire:

Fannie and Freddie could reverse course on principal reductions

Negative equity gap nears $4 trillion

BofaA offers distressed homeowners a chance to stay in homes

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

See celebrity real estate.

Permalink | Email this | Comments

cost of funds index (COFI) loan origination hazard insurance construction loan PUD (Planned Unit Development) recording prepayment penalty

Home Equity Line Adds New Option to Refinancing

Filed under: Home Equity

If you’re looking to refinance your mortgage but you also need some extra cash, there may be a few options out there you haven’t considered. Today’s re-fi rates are low, but to get the best deal overall, your best bet may be to refinance your principal loan at the lowest rate you can find and then to apply for a home equity line for the cash. That way, with today’s low home equity rates, you’ll

If you’re looking to refinance your mortgage but you also need some extra cash, there may be a few options out there you haven’t considered. Today’s re-fi rates are low, but to get the best deal overall, your best bet may be to refinance your principal loan at the lowest rate you can find and then to apply for a home equity line for the cash.

If you’re looking to refinance your mortgage but you also need some extra cash, there may be a few options out there you haven’t considered. Today’s re-fi rates are low, but to get the best deal overall, your best bet may be to refinance your principal loan at the lowest rate you can find and then to apply for a home equity line for the cash.

That way, with today’s low home equity rates, you’ll get the best interest rates for both portions of your financing.

The other main option is a cash-out refinance, in which the borrower takes additional cash above the loan amount. But that usually means an additional 0.5 percent or more in interest, which can add up to thousands of dollars over the course of a 30-year loan. Instead, simply refinance the balance of your mortgage, and then apply for a home equity line for the rest.

Right now, home equity rates are at prime or prime plus 0.5 percent to 1.0 percent, a lot better than almost any other kind of loan out there, including personal loans and credit card debt.

Cash-out refinancing is not a real option for homeowners who are underwater and need to borrow more than 80 percent of the value of their home. And while there are 95 percent loan-to-value mortgages out there, you can’t be living in a declining market such as Arizona, California, Florida, Michigan and Nevada. Also, if your credit score is below 680, you’ll need to turn to the FHA for the refinance if you want anything more than a 90 percent loan-to-value mortgage.

Generally in today’s market, even if you don’t live in a declining market, you probably won’t be able to get an equity line if it means going above 90 percent loan-to-value. And even that could be difficult, unless you have a credit score over 760. Therefore, home equity lines are a better choice for smaller projects, like making needed repairs on your home.

Also, think twice before paying off credit card debt with a home equity line. While you may be paying a high price for credit card debt, transferring credit card debt to an equity line means you are exchanging unsecured debt (debt that is not guaranteed by an asset) for secured debt (in this case debt that is secured by your home). That means, if for some reason you can’t make the payment on your equity line, the lender has the right to foreclose on your home. You can learn more about how equity lines work in the Federal Reserve’s pamphlet “What you should know about Home Equity Lines of Credit.”

Millions of people put their homes at risk because they used the equity in their homes as a piggy bank and borrowed to levels that are now higher than what their homes are worth. Some have walked away from these homes because the combined mortgage and equity line is higher than what the home’s value is expected to be for 10 or 20 years.

But if you need the cash, and it will put you in a better position financially, you’re better off choosing an home equity line than a cash-out refinance.

Lita Epstein has written more than 25 books including The Complete Idiot’s Guide to Personal Bankruptcy and The Complete Idiot’s Guide to Improving Your Credit Score.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2010/12/09/home-equity-line-adds-new-option-to-refinancing/

home inspection lock-in period trustee effective age credit repository loan servicing legal description

Robo-signing settlement may boost short sales

The government’s $25 billion settlement with the nation’s five biggest mortgage servicers over so-called “robo-signing” practices could boost short sales, as loan servicers will receive credit when they approve sales that include forgiveness of a portion of underwater homeowners’ debt.

Although the settlement is only expected to help a fraction of homeowners who owe more their properties are worth — perhaps one in 20, according to one estimate — it will also help bring certainty back to housing markets by removing some of the obstacles that have been keeping homes stuck in the foreclosure pipeline.

Announced last month, detailed terms of the agreement between mortgage servicers and a coalition of state attorneys general and federal agencies were filed today.

http://www.shutterstock.com/gallery-100760p1.html">Andy Dean Photography</a>/<a href="http://www.shutterstock.com">Shutterstock</a>” />

http://www.shutterstock.com/gallery-100760p1.html">Andy Dean Photography</a>/<a href="http://www.shutterstock.com">Shutterstock</a>” />

Broadly, the settlement calls for mortgage servicers to pay $5 billion in fines and commit to a minimum of $17 billion in homeowner relief, including principal reductions. Another $3 billion is earmarked for helping underwater borrowers refinance.

“We will see an increase in short sales, because lenders and loan servicers will get the same credit for doing a short sale, as if they did a loan modification or principal reduction,” said Rick Sharga, executive vice president of Carrington Mortgage Holdings LLC.

The Wall Street Journal reported Sunday that the structure of mortgage write-downs was a major point of contention in the year-long negotiations leading to the settlement.

Allowing debt forgiveness on approved short sales to count against the required $17 billion in principal reductions helped secure a settlement that will reach more borrowers, the paper said. Loan servicers will also get partial credit even when it’s investors, rather than the banks themselves, taking the loss, the Journal said.

A researcher at the Brookings Institution told the Journal that the settlement could help about 5 percent of underwater borrowers, or about 500,000 homeowners.

“We will probably see a short-term increase in forcelosure activity, because the servicers and lenders at last have a sense of certainty about what they can and cant do,” Sharga told Inman News. Part of that increase will also be among loans that don’t meet the criteria of the agreement.

For loan servicers to get credit for a principal reduction, a loan must be at least 30 days delinquent, have a pre-modification loan-to-value (LTV) ratio of at least 100 percent, satisfy specified debt-to-income ratios (DTIs), according to ananalysis of the settlement by the lawfirm K&L Gates. At least 85 of occupied properties must have had an outstanding principal balance at or below the highest Fannie Mae and Fanni Freddie conforming loan limit cap as of January 1, 2010.

Because servicers won’t get 100 percent credit for all types of relief that are provided, the actual amount of relief provided could total as much as 32 billion, state attorneys general said in announcing the settlement.

“In terms of the overall housing market , our position is this will have very little effect on anything,” Sharga said. “Consumer advocates don’t think it went far enough, and people who look at housing markets realize that the number of properties and the amount of money involved won’t have a measurable effect on markets.”

Federal housing officials addressed those and other concerns today.

“This agreement does not — and is not intended to — solve or resolve all the issues and abuses related to the housing crisis,” officials with the Department of Housing and Urban Development blogged today. “This agreement is very narrow as to what it releases banks from. This settlement is intended to address the servicing aspect of the crisis, which did not cause the housing crisis.”

The settlement doesn’t prevent the government from punishing wrongful securitization conduct that will be the focus of the new Residential Mortgage-Backed Securities Working Group, HUD noted. State and federal authorities can also pursue criminal enforcement actions related to conduct by servicers, including civil rights, fair housing, fair lending and other violations.

Also, if the remaining six to 14 loan servicers sign on to the settlement, it would grow to about $30 billion with more than $45 billion in benefit to homeowners, HUD said.

Cade Holleman, executive director of the Irvine, Calif.-based National Association of Women REO Brokerages, said the day is fast approaching when brokers and agents who have concentrated heavily in real-estate owned properties will have to diversify.

Short sales, refinancings, and loan modifications are each “pulling REO inventory out of the game,” he said.

“You’ve got to keep your eye on that process,” Holleman said.”You can no longer be 80 percent REO,” but must diversify into short sales and property management.

merged credit report second mortgage qualifying ratios easement PITI adjustable-rate mortgage (ARM) replacement reserve fund

Case-Shiller: Why the Sky Isn’t Falling

Filed under: Buying, Economy, Financing, Selling, Credit

Count me among the unpanicked over the Standard & Poor’s/Case-Shiller monthly housing index that shows housing values have dipped past a low set during the Great Recession. I’m not even getting goosebumps over the chilling words “housing double-dip.”

Count me among the unpanicked over the Standard & Poor’s/Case-Shiller monthly housing index that shows housing values have dipped past a low set during the Great Recession. I’m not even getting goosebumps over the chilling words “housing double-dip.”

Nope. For the 70 million home-owning Americans who don’t have a need to sell their homes at the moment, this is not the end of the world. Yes, they can thank their lucky stars that they still have jobs and didn’t get ensnared in a toxic mortgage. And yes, they can feel for their friends and family who weren’t so fortunate — or, if they are feeling less charitable, weren’t as smart as they. But for the bulk of Americans, this is a problem that, well, doesn’t hit that close to home.

Want perspective? Of the 75 million owner-occupied homes in the U.S., about 5 million were sold in the past year, which means that there were tens of millions of home owners who were content to stay put, paying their bills and living obliviously to the drops in home prices. Of those five million sales last year, about one third were distressed sales.

Currently, there are 3.87 million homes on the market. In April, distressed homes were 37 percent of sales (24 percent foreclosures and 13 percent short sales). And 7 percent of new listings were foreclosures, but they’ve been entering the pipeline at a steady pace and selling quickly at bargain prices, says the National Association of Realtors.

Of course, scary Case-Shiller numbers are nothing new. Since last June, when a yearlong rebound in prices began to sputter out, the index has recorded losses every month. If there’s a bright spot, it’s that in the last quarterly report, all 20 cities tracked showed declines; in the most recent index, two of the 20 actually showed month-over-month improvement.

And for the record, the experts back in December offered the same explanations as did the experts commenting on this week’s report: The large number of foreclosures on the market and the expiration of the federal homebuyer tax credit are pushing prices down.

I’d throw in an even larger reason that the experts gloss over: Lenders aren’t lending money to even qualified buyers. They have imposed unrealistic standards for those applying for mortgages and then wonder where all the buyers are. Maybe they should look for them under the mountains of paperwork that they keep demanding and misplacing. Seriously, has anyone tried to get so much as a refinance lately?

NAR says, albeit more politely than I do, that “the recovery is uneven, held back by unnecessarily tight credit.” The association projects that “if the lending community simply returned to the safe, sound standards that were in place a decade ago (before the lax standards that led to the unprecedented boom-and-bust cycle), home sales would rise 15 to 20 percent over current projections.” Now wouldn’t that be nice?

These AOL Real Estate guides can help, no matter whether you choose to buy or sell:

- First-Time Homebuyer’s Guide

- How to Shop for Your First Home

- How to Price a Home to Sell Fast

- How to Get a Low Mortgage Rate

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Get property tax help from our experts.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2011/06/02/case-shiller-the-sky-isnt-falling/

convertible ARM mortgagee clear title no-cost loan refinance transaction two- to four-family property adjustment date

5 Cheap Home Security Tricks to Keep Your House Safe

Filed under: News, Advice, How To

![]()

You don’t have to install a pricey or crazy security system to feel safer in your home. Here are some low- and no-cost ways to keep burglars at bay.

1. Don’t Sleep Alone

If you’re sleeping solo these days, take your car’s remote control to bed with you. If you hear suspicious noises, push the remote’s “panic” button and let the alarm scare away intruders.

2. Fake It

Pretend you’re home watching “Downton Abbey” and deter burglars with FakeTV ($34), a small gizmo that glows and flashes like the flicker of a television set. FakeTV uses the same energy as a nightlight, and has a built-in light sensor and timer, which turns it on at dusk and off when you wish.

3. Slippery When Wet

In the U.K., they slather “anti-climb” paint, which never dries, on downspouts, gutters, and anything they don’t want an intruder to shimmy up. It doesn’t seem to be available in the U.S. yet. But it’s a wild idea.

4. Footsteps in the Snow

Virgin snow is a sure sign that no one’s home. If you’re away after a snowstorm, ask a neighbor’s kid to tromp around your yard, creating footprints that will fool a burglar into thinking you’re around but just haven’t gotten around to shoveling your snow yet.

5. Parked Car

Also, ask a neighbor to occasionally park their car in front of your house, making it look like you’re entertaining visitors. And ask them to remove any fliers that may be wedged into your door or mailbox. Burglars sometimes case a home by planting a flier and checking to see if someone retrieves it.

This story was originally published on HouseLogic.

See more on HouseLogic:

6 Household Hacks Inspired by MacGyver

Want to Add Sconce Lighting?

Fragrant Plants That Will Keep Your Home Smelling Good

%Gallery-114116%

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/10/03/cheap-home-security-tricks-to-keep-your-house-safe/

cash-out refinance depreciation merged credit report second mortgage qualifying ratios easement PITI

10 DIY Projects That Even Renters Can Do

Filed under: News, Home Improvement, How To

By Scott Gamm

By Scott GammNEW YORK — Even though mortgage rates are at historically low levels, it’s the rental market in many areas across the U.S. that is really heating up. Obtaining a mortgage is undoubtedly a strenuous process on the heels of tightened credit standards. Add to that the fact that many Americans simply can’t afford a new home, the number of Americans still jobless or just getting by — and many consumers are finding it easier, or necessary, to rent, which explains why the average rent nationally is at its highest level since 2007, according to researchers at Reis.

Testifying on Capitol Hill in the aftermath of the housing crash, Treasury Secretary Timothy Geithner spoke words that previously might have been considered political suicide: Geithner suggested that homeownership should no longer be considered a singular measure of the American Dream — and maybe every American shouldn’t own a home.

Welcome to the post-housing bubble renter’s society. Geithner didn’t mention it, but his words implied that the do-it-yourself projects associated with the American Dream of home ownership should be applicable to the growing ranks of renters across the nation.

When renting, it doesn’t make sense to complete a major renovation, like flooring, new windows or a new kitchen. Throughout the duration of your lease, however, there are some easy and inexpensive projects you can do yourself to spruce up your rental. MainStreet asked design pros to weigh in on the top DIY projects for renters.

Replacing a Showerhead

If you’ve ever thought the weak water pressure in your shower has nothing to do with the low-flow showerhead installed by the building to minimize their water bill, think again. Chances are the showerhead in your rental needs to be replaced — whether or not it’s because the landlord installed a low-flow head. You, and your hair, will be very happy if you complete this project, and thankfully, this isn’t a lengthy or costly job.

First off, it’s helpful to know the types of showerheads so you can easily narrow your choices when selecting one at a home improvement store.

“There are two main categories of showerheads to choose from: fixed or handheld. But within these categories is a wealth of options — from rainshowers to multi-setting versions,” said Andrea Conroy, director of retail marketing at Moen.

And as for the actual installation of your new showerhead, here’s what Controy suggests:

1. Unscrew the existing showerhead from the shower arm, using a crescent wrench if necessary.

2. Remove any old thread seal tape and apply new by wrapping the tape around the shower arm threads two to three times.

3. By hand, screw the new showerhead onto the shower arm. Use the wrench to tighten the new showerhead. If installing a handheld version, first screw the handheld bracket to the shower arm and tighten with a wrench. Then, attach the hose and handheld shower to the handheld bracket.

Choosing the Right Paint Color

Any time you move into a new place, chances are you’ll be painting the kitchen, bedrooms and living room. When choosing what color to paint your rental, there’s a “science” behind different colors.

“Blue colors elicit feelings of tranquility and confidence. This is the least appetizing color, so it should not be the main color in a kitchen,” advises Chris Ring, v.p. of ProTect Painters.

“Yellow enhances concentration, speeds metabolism, and is perfect for kitchens and bathrooms,” Ring advises.

Pink colors are on the tranquilizing end of the color mood scale, making a pink shade an appropriate choice for bedrooms.

For this and other painting tips below, do keep in mind that even if you are a Michaelangelo, you may have to repaint the walls to white when you move out, and/or take the risk of a landlord trying to claim part of a security deposit as a result of a custom paint job. As such, it’s best to ask for a landlord’s approval to paint and agree to terms before undertaking the project.

Painting the Bathroom

Painting a tiny bathroom makes for a challenge, especially when trying to paint around the sink, mirror and shower.

“Before painting, wash all the walls to remove any mildew with mildew remover or bleach and water,” advises Joe Kowalski, training manager at Glidden.

And for your bathroom painting job, Kowalski adds these recommendations:

- For walls, use either a semi-gloss or eggshell finish; both provide dirt and moisture resistance.

- For the ceiling, paint with an eggshell finish is advised.

- Paint that includes primer provides extra adhesion over a glossy surface.

More Storage Is Better

Whether you’re sidestepping into your small studio rental or fortunate enough to be renting a place with enough closet space, tips for maximizing your rental’s storage space always come in handy.

Janet Lee, author of Living In A Nutshell, shares these tips:

1. Place a removable, peel-and-stick wall decal on a bare surface (whether it’s on a wall or the back of a door.)

2. Rub the surface of the sticker with a squeegee to ensure that the decal lays smoothly against the wall.

3. Add a hook onto the decal and apply pressure to ensure damage-free hanging.

4. Wait one hour before hanging hats, jackets, backpacks and other apparel.

Hiding Your Lamp Cord

Cords can make your rental a cluttered mess as well as an electrical hazard for children. Lee offers these easy steps for making the cord “disappear”:

1. Use a hand drill to create a hole in the bottom of a metal gelatin mold.

2. Run a pre-wired pendant cord through the hole of the mold.

3. Insert a light bulb into the end of the cord.

4. Affix cords to wall in decorative loops using clear cord clips for damage-free hanging.

Read the rest of this story at TheStreet.com.

More from TheStreet:

Kids Off to College? Time to Sell Your Home

10 DIY Projects for Your New Home

10 Home Improvements You’re Wasting Time and Money On

%Gallery-159150%

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/07/23/10-diy-projects-that-renters-can-do/

merged credit report second mortgage qualifying ratios easement PITI

Obama: Mortgage Help Coming for Military, FHA Borrowers

Filed under: News, Foreclosures, Refinancing

WASHINGTON — President Barack Obama is aiming mortgage relief at members of the military as well as homeowners with government-insured loans, the administration’s latest efforts to address a persistent housing crisis.

In his first full news conference of the year Tuesday, Obama was to announce plans to let borrowers with mortgages insured by the Federal Housing Administration refinance at lower rates, saving the average homeowner more than $1,000 a year. Obama also was detailing an agreement with major lenders to compensate service members and veterans who were wrongfully foreclosed upon or denied lower interest rates.

A senior administration official described Obama’s proposals to The Associated Press, ahead of the announcement, on the condition of anonymity.

The efforts Obama is announcing do not require congressional approval and are limited in comparison with the vast expansion of government assistance to homeowners that he asked Congress to approve last month. That $5 billion to $10 billion plan would make it easier for more borrowers with burdensome mortgages to refinance their loans.

Lower Refinancing Fee

Under the housing plans that Obama was to announce Tuesday, FHA-insured borrowers would be able to refinance their loans at half the fee that the FHA currently charges. FHA borrowers who want to refinance now must pay a fee of 1.15 percent of their balance every year. Officials say those fees make refinancing unappealing to many borrowers. The new plan will reduce that charge to 0.55 percent.

With mortgage rates at about 4 percent, the administration estimates a typical FHA borrower with $175,000 still owed on a home could reduce monthly payments to $915 a month and save $100 a month more than the borrower would have under current FHA fees.

Though 2 million to 3 million borrowers would be eligible, the administration official would not speculate how many would actually seek to benefit from the program. The FHA provides mortgage insurance on loans made by FHA-approved lenders throughout the United States and its territories. The loans typically go to homeowners who do not have enough equity to qualify for standard mortgages. It is the largest insurer of mortgages in the world.

Review of Vets’ Foreclosures

For service members and veterans, Obama will announce that major lenders will review foreclosures to determine whether they were done properly. If wrongly foreclosed upon, service members and veterans would be paid their lost equity and also be entitled to an additional $116,785 in compensation. That was a figure reached through an agreement with major lenders by the federal government and 49 state attorneys general.

Under the agreement, the lenders also would compensate service members who lost value in their homes when they were forced to sell them due to a military reassignment.

Obama is holding the news conference in the midst of a modestly improving economy. But international challenges as well as a stubbornly depressed housing market remain threats to the current recovery and to his presidency.

Obama has not held a full news conference since November. The White House scheduled this one on the same day as the 10-state Super Tuesday Republican presidential nominating contests. While aides insisted the timing was coincidental, it follows a pattern of Obama seeking the limelight when the attention is on the GOP.

The news conference comes amid a new sense of optimism at the White House. Obama’s public approval ratings have inched up close to 50 percent. The president recently won an extension of a payroll tax cut that was a main element of his jobs plan for 2012. Economic signals suggest a recovery that is taking hold.

Still, he will probably face questions about the pace of the recovery. The unemployment rate in January was 8.3 percent, the highest it has been in an election year since the Great Depression. With rising gasoline prices threatening to slow the economy, Obama has also faced attacks from Republicans over his energy policy.

Iran’s nuclear ambitions will also command attention in the aftermath of his meeting Monday with Israeli Prime Minister Benjamin Netanyahu. Tension over Iran has already contributed to higher oil prices, and Israel’s threats of pre-emptive military strikes to prevent Tehran from building a nuclear bomb have dominated Washington discourse for weeks.

Other developments in the Middle East, where turmoil has soured some of the promise of last year’s Arab Spring, are also likely to be addressed. Syria’s bloody crackdown on protesters has increased pressure on Obama to intervene. Republican Sen. John McCain on Monday urged the United States to launch airstrikes against Syrian President Bashar Assad’s regime to force him out of power.

Copyright 2012 The Associated Press. The information contained in the AP news report may not be published, broadcast, rewritten or otherwise distributed without the prior written authority of The Associated Press. Active hyperlinks have been inserted by AOL.

Also see:

Only 5% of Underwater Homes May Qualify for Write-Downs

REO to Rental: Fannie Mae Dips Further Into Foreclosure Pool

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/03/06/obama-mortgage-help-coming-for-military-fha-borrowers/

adjustable-rate mortgage (ARM) replacement reserve fund deed certificate of deposit lease purchase money transaction closing costs

More Americans Consider Strategic Default on Mortgages an Acceptable Option

Filed under: News, Economy, Financing

After years of economic turmoil faced by millions of Americans, a large number of consumers now have new attitudes toward the kinds of financial missteps that can land borrowers in credit trouble, including strategic defaults.

After years of economic turmoil faced by millions of Americans, a large number of consumers now have new attitudes toward the kinds of financial missteps that can land borrowers in credit trouble, including strategic defaults.

A sizable amount of Americans now consider it socially acceptable to have a low credit score or strategically default on their outstanding mortgage balances, according to new data compiled by JZ Analytics as part of a poll for ID Analytics. In all, 36 percent of those polled said they believe it’s acceptable to have a poor credit score these days, accounting for 77 million people across the country if the data is extrapolated out.

More interesting, however, is that many consumers have seen their attitudes toward intentionally falling behind on underwater mortgages change drastically in the last few years, the report said. A total of 32 percent of those polled — 68 million people nationwide — say homeowners should be able to strategically default on their mortgages without facing any consequences whatsoever for doing so.

Further, 13 percent, or 28 million Americans, say they would likely strategically default, the report said. Another 17 percent, or 36 million residents, say they know people who have already done so.

“Our research into the consumer opinion of the economic crisis of 2008 found alarming results,” said John Zogby, a senior analyst at JZ Analytics and creator of the Zogby Poll. “What jumped out is how many Americans feel it is acceptable for homeowners to walk away from a mortgage and go into foreclosure. If Americans carry on with that mindset, it will continue to cause problems as the economy undergoes a slow recovery.”

Another area in which consumers have more relaxed attitudes toward certain aspects of their credit rating is whether they would exaggerate their standing to obtain new lines of credit, the report said. In all, 17 percent of those polled said they would do so, making up some 36 million Americans.

Finally, another 35 percent of respondents — 75 million Americans in all — said they are now more afraid of being victimized by identity theft than they were five years ago, the report said.

Identity theft and account mismanagement can lead to serious damage to a borrower’s credit score, and therefore all financial documents, including credit reports, should be monitored closely as often as possible.

See more on Credit.com:

How Often Does Your Credit Report Change?

5 Reasons Why Your Credit Score May Not Matter

The Ultimate Credit Report Cheat Sheet

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

bond market servicer appraisal owner financing due-on-sale provision asset application

Mortgage Principal Reduction on Freddie Mac Loans?

By Jon Prior

Freddie Mac CEO Charles “Ed” Haldeman gave a strong signal Friday that new incentives from the Treasury Department may be enough to start principal reduction on mortgages backed by the government-sponsored enterprises.

In January, the Treasury said it would triple incentive payments to mortgage investors who allow principal reduction in Home Affordable Modification Program workouts. The payouts ranged between six and 21 cents to the investors for each dollar forgiven under HAMP, but that will grow to between 18 and 63 cents.

“I have to say recently the Treasury sweetened the program and tremendously increased the incentive payments in their offer to us,” Haldeman said at HousingWire’s REThink Symposium. “We will reevaluate that to see what may be in our economic best interest. If there are very large incentive payments — which could be 50 percent of what you could write down — it may be in our economic self-interest to participate in that.”

There are currently 11.1 million borrowers who owe more on their mortgage than the house is worth, according to CoreLogic. Of that, estimates show roughly 3.3 million of those mortgages belong to Fannie and Freddie.

The GSEs and their regulator, the Federal Housing Finance Agency, long shunned principal reduction. Their biggest fear is moral hazard — that borrowers who are still current on their underwater loan would strategically default in order to get principal written down.

“We thought principal reduction could have unintended, secondary consequences on other borrowers seeking the same kind of reduction,” Haldeman said.

One previous analysis showed the GSEs would take significant credit losses if a wide-scale program was put in place. A new analysis from the FHFA, which would cover the new HAMP incentives, is expected to be released in the coming weeks.

NPR and ProPublica reported Friday that the analysis will show a reversal, that principal reduction will work for the GSEs under the new version of HAMP.

“As we complete the review, the public should understand that Fannie Mae and Freddie Mac continue to offer a broad array of assistance to troubled borrowers and have continued to implement HARP 2.0 to enhance refinancing opportunities for underwater borrowers,” FHFA said in a statement.

Treasury Secretary Timothy Geithner told a House panel this week he and FHFA Acting Director Edward DeMarco were working out their differences.

Haldeman, who announced in October that he would leave his post at Freddie, said the principal reduction verdict will ultimately reside with DeMarco, but he isn’t operating on his own.

“At the end of the day, we are in conservatorship, and he is the conservator. But the way it works on a day-to-day basis is that it’s a very close collaboration. It is extremely rare that I had a different point of view than Ed DeMarco,” Haldeman said.

Read more on HousingWire:

Fannie and Freddie could reverse course on principal reductions

Negative equity gap nears $4 trillion

BofaA offers distressed homeowners a chance to stay in homes

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

See celebrity real estate.

Permalink | Email this | Comments

appraised value escrow account grantee Government National Mortgage Association (Ginnie Mae) closing Fair Credit Reporting Act Real Estate Settlement Procedures Act (RESPA)

‘Housing’ Swings Don’t Matter as Much as What’s Happening in Your Own Neighborhood

Filed under: News, Advice, Economy

By Jeff Brown, BankingMyWay

By Jeff Brown, BankingMyWay

NEW YORK — New data from Zillow.com shows that the housing market really has hit bottom. Cue the applause. Signal the all clear. Get Warren Buffett to pile on and say something encouraging about the U.S. economy. Then head back to reality, and eye the headlines about the housing market’s inevitable recovery with caution, especially if you are a prospective homebuyer. Conditions can vary widely from one neighborhood to the next.

The question isn’t ever whether the market has bottomed when it comes to housing — that’s good for journalists and economists and TV pundits, but near-useless, or at least dubious, for those involved in or contemplating real estate transactions. The relevant question is whether the market has bottomed in your neighborhood.

All politics are local — all real estate, too. So local, in fact, that the outlook for your metro area can matter less than the outlook for your five-digit ZIP Code (and vice versa: improving home values in a specific ZIP Code don’t imply that an overall metro area is on the mend, too). And sometimes, improvement within a ZIP Code doesn’t mean the home in that ZIP Code you are interested in — or looking to sell — is in the improving part of the “code.”

As Zillow puts it in the details of calling a bottom in the housing market, “The recovery is a highly local process.” Still the headlines won’t ever say, “(Highly Local) Housing Market Hits Bottom.”

This isn’t to say the news on housing isn’t good, especially for some of the most underwater markets:

“The United States has hit a bottom in housing values, and a majority of metros that the Zillow Real Estate Market Reports cover have also experienced their bottom,” Zillow’s recent report states. “Some metros showed signs of a healthy pick-up in appreciation, such as Phoenix and Miami with a V-shaped recovery. Others are undergoing more of a soft landing and are currently coasting in positive value growth territory.”

Zillow compares home prices from June 2011 to June 2012 in 167 metropolitan areas, with breakdowns by ZIP Code. While the results are encouraging overall, some ZIP Code and metro areas continue to fare poorly. Zillow uses red to show where prices have fallen and green for where they’ve gone up. In addition to the year-over-year maps, there are maps showing price trends in the most recent quarter and month. Using these visual aids, one can see, for example, that a positive trend over the past year has not been reversed in recent months.

So how can one make use of the data? By zeroing in on individual ZIP Code, prospective buyers can assess the risk that a home bought today might be worth less in a year or two — a good reason to postpone a purchase. There’s no way of knowing for sure, but if prices have been holding steady or begun to rise, the area is a better bet than if they are continuing to fall.

Similarly, signs of an upturn might encourage sellers to get off the sidelines and list their properties. If the market warms, there are likely to be more buyers willing to move quickly before prices rise even more. Of course, a prospective seller who’s not in a hurry might be wise to wait for prices to go even higher.

Still, it’s important to keep data in perspective. Like most surveys of this type, Zillow calculates average prices of homes sold in a given area during a given period. If only a small number of homes sell, the results can be skewed by just a few sales with especially high or low prices. Don’t put too much stock into a trend that’s only evident for the past month or quarter, as there may not have been enough sales to guarantee a statistically significant result.

The ideal survey would look at prices of individual homes that have changed hands more than once, but not many homes sell more than once in a 12-month period, so average prices for the area are generally the best data available.

People using the data should also keep in mind that a ZIP Code-level look is really not detailed enough, as a given ZIP Code will have many neighborhoods quite different from one another. Before making a final decision to buy or sell, look carefully at comparable homes that have sold, or are on the market, in the same neighborhood.

So when you read the next headline calling a bottom in the U.S. housing market, it would be best to ignore it as anything other than a way to re-frame the debate and begin the real detailed work of answering the more important question: Does that call apply to your neighborhood?

See more at TheStreet.com:

Kids Off to College? Time to Sell Your Home

10 DIY Projects for Your New Home

10 Home Improvements You’re Wasting Time and Money On

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

appraisal owner financing due-on-sale provision asset application common area assessments cost of funds index (COFI)

HARP Now Expected to Reach Twice as Many Homeowners

Filed under: News, Refinancing

The expanded Home Affordable Refinance Program will likely reach more underwater borrowers than its architects originally thought.

“We said we would double the number from what we’ve already done under HARP, which would mean we’d do another 900,000 under the expanded program. I think we’re actually trending above that now,” said Andrew Bon Salle, head of the Fannie Mae underwriting and pricing group, in an interview.

%Gallery-158524%

The Federal Housing Finance Agency eased HARP eligibility requirements last year for Fannie Mae and Freddie Mac mortgages. It reduced upfront fees, eased buyback risk and eliminated the 125 percent loan-to-value ratio ceiling. Most banks implemented the changes in March.

Read more on this story at HousingWire.

More on AOL Real Estate:

Find out how to calculate mortgage payments.

Find homes for sale in your area.

Find foreclosures in your area.

Find homes for rent in your area.

Follow us on Twitter at @AOLRealEstate or connect with AOL Real Estate on Facebook.

Permalink | Email this | Comments

Source: http://realestate.aol.com/blog/2012/06/25/harp-architects-expect-to-reach-1-million-more-homeowners/

cooperative (co-op) title search collection contingency first mortgage assessor exclusive listing

Renting is Easy

There are times when we need an extra space for our need. However, we do not have enough money to buy a new place. This way we need to rent place. Of course, there are many things that we need to consider when we are renting a place. Often we encounter that renting a place […]

Source: http://www.brothernwla.org/renting-is-easy/

bond market servicer appraisal owner financing due-on-sale provision asset application

Mortgage Points: When It’s Smart to Pay More Upfront

Filed under: News, Advice, Financing

Pay more now for a chance to save much more later? That’s the idea behind paying “points” on a mortgage loan. But it doesn’t necessarily make sense for every homeowner.

Mortgage points provide an opportunity for borrowers to lower their monthly mortgage payments by paying a lump sum at a loan’s closing in exchange for a lower mortgage interest rate over the course of a loan.

Mortgage points are a smart option for borrowers who plan to stay in the same mortgage and not refinance for a relatively long period of time. But points are not recommended for borrowers who are likely to relocate or refinance in the not-so-distant future.

Borrowers pay points in order to lower their mortgage interest rates by a certain amount. The cost of one point is equal to one percent of the mortgage amount. In the case of a 30-year fixed-rate mortgage, paying one point will typically lower your interest rate by somewhere around one eighth of a percent, according to Tim Dwyer, chief executive officer of Entitle Direct, a title insurance company.

So if borrower A paid one point on a $200,000 mortgage with what would have been a 4 percent interest rate, she would lower her interest rate to 3.875 percent (4 percent — 1/8th percent) for the cost of $2,000.

A good way of looking at points is to view them as an investment that “yields a return for the longer you stay in your house,” mortgage expert Jack Guttentag writes.

If Borrower A stays in the same mortgage for only a few years before selling her home or refinancing, she may end up not saving enough in monthly payments to justify paying the $2,000 upfront. But if she stays in the mortgage for a longer period of time, she eventually breaks even on her investment and enjoys saving money every month from there on out.

“If the points are reasonable, I want to pay that upfront and enjoy the interest rate savings over 10 years because I know I’m not going to refinance,” Dwyer says. But if “you’re a young couple” and “you know you’re going to have more babies, you know you’re going to be moving out,” then you should avoid paying points.

Banks may offer 10 or more point combinations on any given loan, Guttentag writes, and borrowers often don’t end up selecting the option that aligns most with their interests, simply out of ignorance. You can use a point calculator to find out how long it would take to break even using different point combinations.

In a perfect world, borrowers would pay points only if it benefited them in the long run. But, in fact, many borrowers pay points out of necessity. Why?

Lenders will only allow borrowers’ monthly mortgage payments to equal up to a certain percentage of their monthly income. Often they will only approve loans for borrowers whose monthly mortgage payments would not exceed 28 percent of a borrower’s monthly income.